With a potential wave of CLO supply hitting the market in October, largely from refinancing and reset transactions of existing deals, investors are preparing for a spread widening event. While it is almost assured that the refinancing and reset calendar will be heavy in October, the overall effect on market spreads is less clear. In this piece, we explore the various dynamics that can impact CLO market spreads, while providing an overview of the mechanisms associated with these CLO transactions.

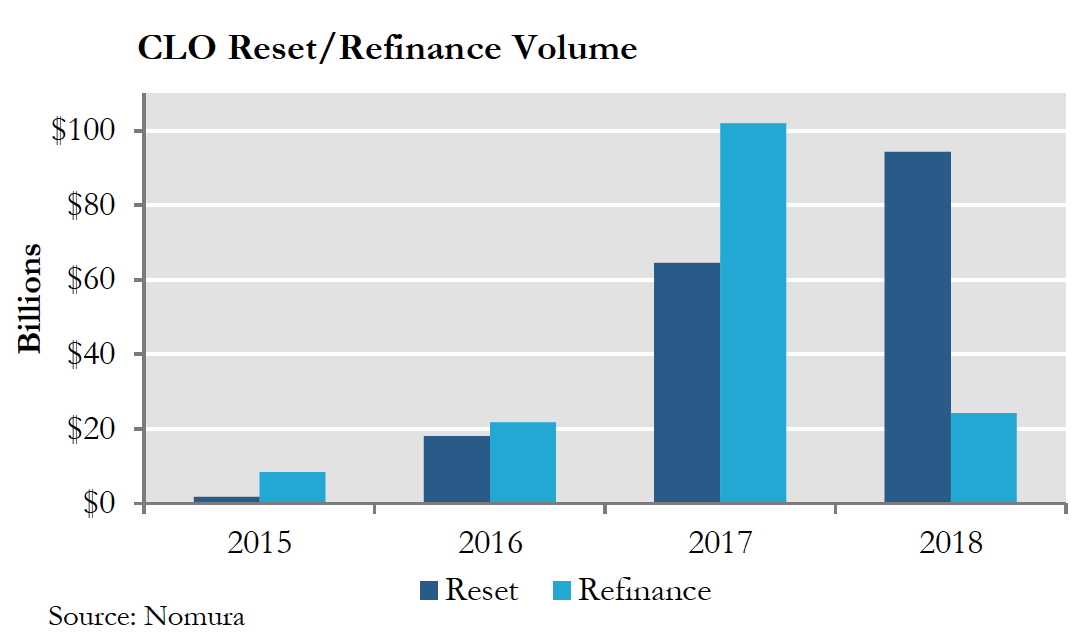

While CLO refinancing and reset transactions are not a new market phenomenon, they picked up in volume dramatically over the last several years as credit spreads tightened. Total volume of these transactions grew from $10 billion in 2015 to $166 billion in 2017. 2018 year-to-date issuance has exceeded $117 billion so far (Figure 1). Although both terms are sometimes used interchangeably, there are key differences between the two transaction types.

In a refinancing, some or all of the existing deal’s liabilities are called and replaced at a lower spread when eligible. The rest of the deal’s structure remains unchanged, including the assets, the reinvestment period end date, and the maturity date. The main purpose of a refinancing is to lower the liability costs of the deal, benefitting the equity holder. It should also be noted that minor changes are sometimes made to the terms of the indenture.

In a refinancing, some or all of the existing deal’s liabilities are called and replaced at a lower spread when eligible. The rest of the deal’s structure remains unchanged, including the assets, the reinvestment period end date, and the maturity date. The main purpose of a refinancing is to lower the liability costs of the deal, benefitting the equity holder. It should also be noted that minor changes are sometimes made to the terms of the indenture.

In a reset, the entire CLO is essentially called and reissued at current market spreads, complete with new terms. While the original special purpose vehicle is retained, the reinvestment period end date and deal maturity date are both extended. The original deal’s assets are carried over, although they can be combined with new assets. Whereas a refinancing is done to lower liability costs, that is not always the case in a reset. The main purpose of a reset is to extend the life of the deal.

In almost all instances, a manager would prefer a reset in lieu of a refinancing. Resets accomplish the same goal as a refinancing in a lower spread environment while extending both the life of the deal and the manager’s fee stream. These incentives changed under the adoption of risk retention rules. As part of the new regulations, CLOs issued before risk retention took effect were subject to the new risk retention rules under a reset transaction, but not under a refinancing in most cases. Given that the majority of CLO managers were either not set up to own their own equity or would be taking lesser fees to do so, refinancing appeared to be the more attractive option in many cases.

The repeal of risk retention earlier this year opened the door for reset transactions. As their 2-year non-call periods come to an end, a large portion of 2016 vintage deals are reaching their refinancing and reset eligibility. Since these deals were done at a time when market spreads were significantly wider than today, deal managers and equity holders are highly incentivized to lower the deal’s liability costs, compounding the potential reset and refinance supply issue. Since many transactions can only occur on deal payment dates, October 15th is the last option for most deals before year-end. Approximately $24 billion of deals are projected to be refinanced or reset on October 15th. To put this in perspective, this is approximately 10% of the total projected yearly supply hitting the market at once.

Although the headline supply number is large, the actual impact on the market may not be as significant as anticipated. The main factor that affects market spreads is not necessarily supply, but rather net supply. When a deal goes through a refinancing or reset, existing securities get redeemed. That redemption leaves investors with cash, which has a high likelihood of being reinvested back into the CLO market. It leaves us with the question of which current CLO investors would be unlikely to reinvest into a refinance or reset transaction and who would only reinvest at wider spreads.

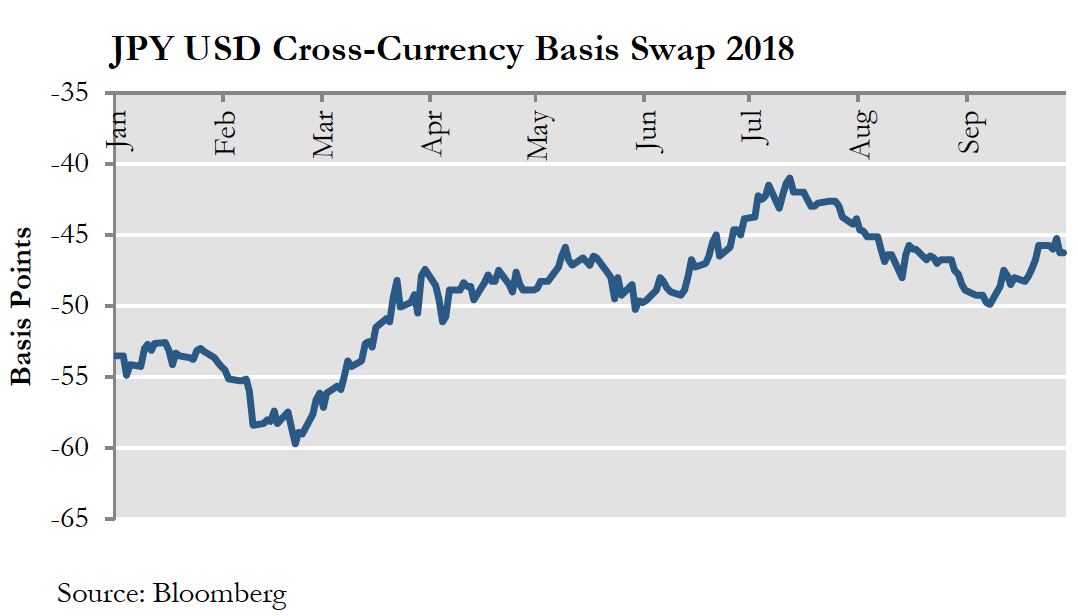

The first answer that comes to mind is foreign purchasers of U.S. CLOs, specifically Japanese institutions who are major buyers of AAA securities. A Japanese investor, like any foreign investor, must analyze U.S. yields adjusted back into their home currency. An increase in currency hedging costs can dampen demand from foreign buyers. This cost increase is exactly what happened earlier this year when JPY-adjusted spreads for AAAs approached 40 basis points for Japanese investors. Since that point, cross-currency basis swap costs have improved for Japanese investors, from approximately -60bps to -46bps as of the end of September (Figure 2). Furthermore, the market expectation of at least two future Federal Reserve interest rate hikes and resulting higher yields of U.S. CLO AAA securities could offset any currency hedging concerns. Japanese investors may not see a better risk-adjusted alternative anywhere else.

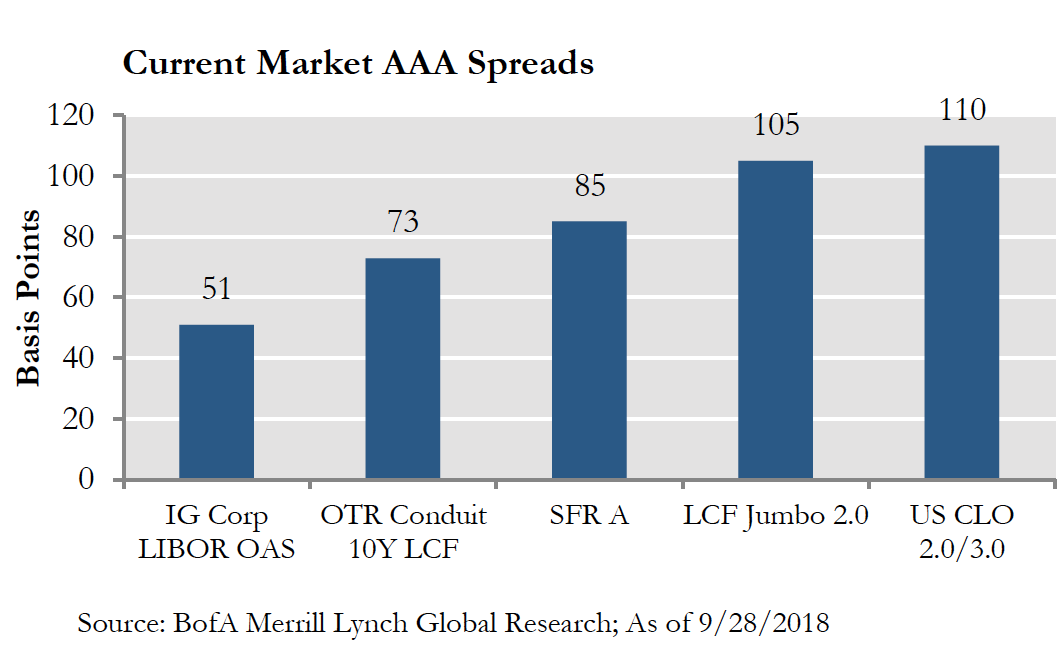

Domestically, U.S. investors could back off current clearing levels in the hope of sourcing cheaper assets given the amount of supply. While this game of chicken between CLO investors and managers could push spreads wider, there are reasons to believe the widening will be limited. For one, CLOs still offer attractive risk-return levels, especially at the top of the capital structure. In fact, among all similar AAA-rated assets, CLOs currently offer the highest spread (Figure 3). Within the structured credit market, there are limited sectors as large as CLOs that offer the same benefits for investment grade accounts (floating rate, significant credit enhancement, minimal historical losses). Investors may not have the stronger hand here as the fear of missing out on this asset class could incentivize them to step up and take down securities as there is still a large amount of money chasing limited assets within the structured credit markets. Additionally, reset transactions come without the ramp-up risk of a brand new CLO given that the bulk of the assets have already been acquired. This lack of ramp-up risk is a desirable characteristic to many investors, making the deals less likely to widen dramatically.

Finally, the potential volume of refinance and reset transactions expected to come to market may be overstated and is likely to decrease as we move forward. Whether it’s obtaining approval of the current equity holder or dealing with rating agency constraints, not all eligible deals will have a seamless path to reissuance. In some cases, if the deal has experienced impairments or poor performance, equity holders may need to inject money into the deal to increase the subordination of the debt tranches to satisfy ratings constraints. Additionally, equity investors may choose to hold off if they believe their cost of financing is too wide and wait for a more opportune supply environment to reissue their debt. Finally, as we look forward and start to consider 2017 vintage deals exiting their non-call periods, lower original liability costs simply make them less attractive candidates for potential refinance or reset transactions, dampening future potential supply.

2018 has seen a record wave of supply so far as managers and equity holders continue to improve their financing terms. While spreads have widened at times around heavy payment date associated periods, the strong demand for CLO debt tranches from a growing investor base should continue to digest the deals that come to market. Major international buyers such as the Japanese are likely to continue to be major buyers of CLO debt as currency hedging costs abate and U.S. rates continue to rise. Domestic investment grade buyers will be hard-pressed to find better risk-adjusted returns elsewhere with features such as floating rates and significant credit enhancement. By and large, the CLO market has weathered supply-driven storms in the past and should continue to do so, even as the volume of refinance and reset transactions picks up in the near term.

Important Notes These materials have been provided for information purposes and reference only and are not intended to be, and must not be, taken as the basis for an investment decision. The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Ellington Income Opportunities Fund. This and other important information about the Fund are contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling 1-855-862-6092. The Prospectus should be read carefully before investing. Princeton Fund Advisors, LLC, and Foreside Fund Services, LLC (the fund’s distributor) are not affiliated. Investing involves risk including the possible loss of principal.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Ellington assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Ellington’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN STRATEGIES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN, INCLUDING INVESTMENT IN COMMODITY INTERESTS, IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS.

Example Analyses Example analyses included herein are for illustrative purposes only and are intended to illustrate Ellington’s analytic approach. They are not and should not be considered a recommendation to purchase or sell any financial instrument or class of financial instruments.

Forward-Looking Statements Some of the statements in these materials constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, estimates, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements in these materials are subject to inherent qualifications and are based on a number of assumptions. The forward-looking statements in these materials involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets in which we plan to trade; (ii) changes in strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in interest rates, the debt securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) increased prepayments of the mortgage and other loans underlying our mortgage-backed or other asset-backed securities; (viii) changes in governmental regulations, tax rates, and similar matters; (ix) changes in generally accepted accounting principles by standard-setting bodies; (x) availability of trading opportunities in mortgage-backed, asset-backed, and other securities, (xi) changes in the customer base for our business, (xii) changes in the competitive landscape within our industry and (xiii) the continued availability to the business of the Ellington resources described herein on reasonable terms.

The forward-looking statements are based on our beliefs, assumptions, and expectations, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of instruments and business discussed herein may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

PRINCF-20190924-0026