The U.S. economy has experienced strong growth in recent years, led in part by a booming housing market that has significantly recovered from the years following the financial crisis. Higher home prices and increased homeowner equity have fueled consumer confidence, serving as a foundation for robust economic growth. However, recent macroeconomic data has indicated potential cracks beginning to form in the housing market, worrying homeowners and investors alike. We dig deeper into the data to get a more accurate view of the various dynamics driving these numbers, showing why we believe that the U.S. housing market is poised to show continued strength, especially in the context of legacy non-agency RMBS.

Reading the current news can lead to a bleak view of U.S. housing. Recent information tells us that housing demand has been hampered as affordability is deteriorating, driven in part by higher interest rates. The 30-year Freddie Mac conforming mortgage survey rate has increased over 50 basis points this year and is poised to go even higher with further rate hikes expected from the Federal Reserve. Home builder stocks have suffered as orders for new homes greatly underperformed expectations. Existing home sales decreased for the 4th straight month in July, leading to bloated inventories. The total for-sale inventory of U.S. existing homes has steadily increased this year and is currently sitting at 1.71 million units. But with such negative news on both the supply and demand fronts, what has been the impact on prices in the market?

The answer is contrary to what these recent data points would lead us to believe. Home prices continue their march upwards in spite of the negative news. The median sales price for existing home sales hit an all-time high in June, up 5.4% from the previous year. We believe there are several factors behind the headline numbers responsible for these price moves.

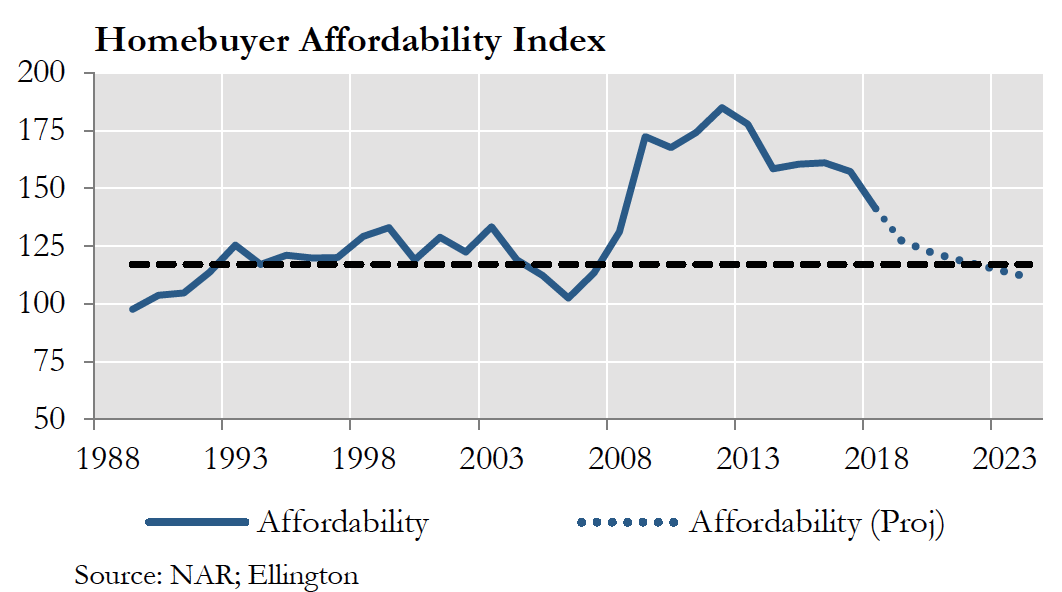

For one, recent information must be viewed in historical context, not simply in terms of the last several years. Even with its recent declines, home affordability is still much higher than its average over the last 30 years. Mortgage rates would have to increase almost 2% from current levels in order for home affordability to simply return to its long-term average. Similarly, assuming home prices continue to grow at 5%, wages continue to grow at 2.5%, and mortgage rates are indexed to Fed Funds futures, we project that homes will remain more affordable than the long-term average prior to the housing bubble through the middle of 2022 (see Figure 1). Existing home inventories are also still well below their average over the last 30 years. While these numbers have come off their recent extremes, they are still at very attractive levels from a historical perspective and continue to support home price growth.

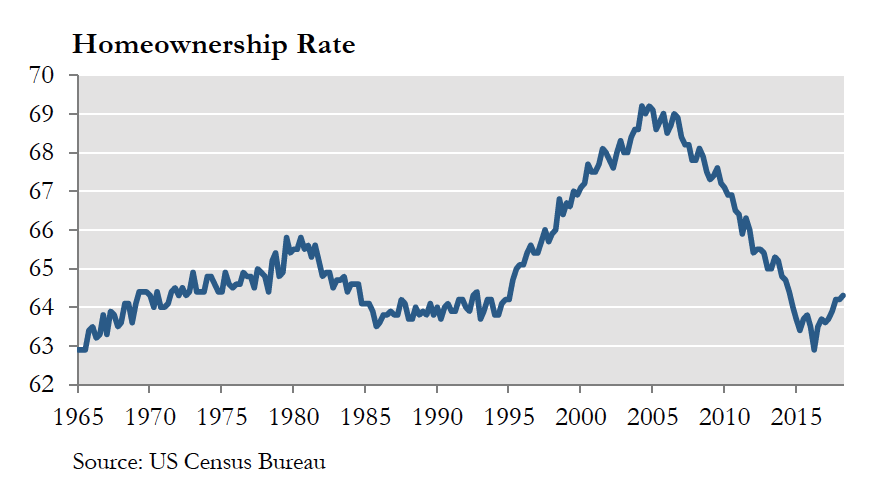

Additionally, strong tailwinds on the demand side of the home price equation work to offset the recent increase in mortgage rates. The U.S. has seen steady growth in household formation, led by an ageing millennial generation. Moreover, these newly formed families are deciding to become homeowners instead of renters. The U.S. homeownership rate has been rising since 2017 as it recovers from the lowest levels seen since the 1960s. This was the first meaningful increase in the U.S. homeownership rate since 2004 (See Figure 2). Although there are many economic factors playing into this, we believe this rebound is partly driven by a tapering of the foreclosure crisis. After seven years, a foreclosure demerit drops off one’s credit report, meaning that millions of borrowers who experienced foreclosures prior to 2012 may now have a higher credit score and thus a higher likelihood of homeownership.

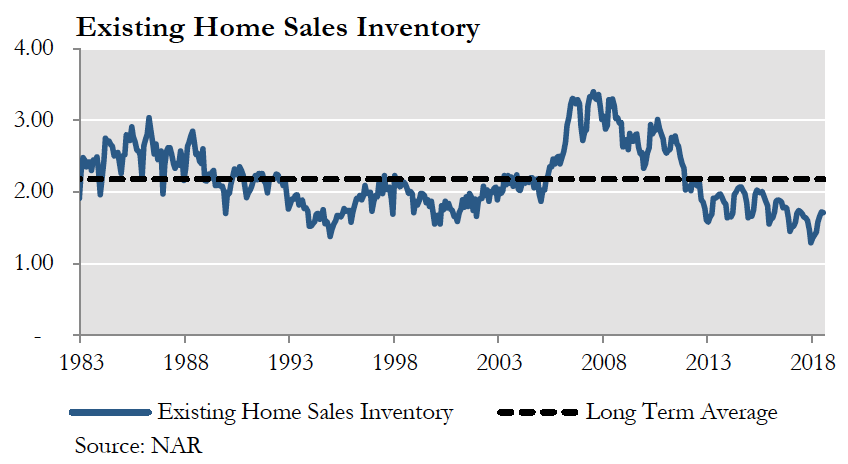

On the supply side, we believe that higher existing home inventories, while still low historically, have been offset by a decrease in new construction (See Figure 3). Home builder stocks have suffered not necessarily because of weakness in the housing market but because of the rising costs associated with building a new home. According to the National Association of Home Builders, 60% of the costs of building a new home are associated with labor and materials, two areas that have been increasing due to continued shortages of skilled laborers along with increasing costs of materials such as lumber.

This brings up another important point for investors. Not every investment that offers exposure to the U.S. housing market comes with the same risks. The home builder sector perfectly illustrates this fact. While the sector is clearly exposed to housing demand, it also is exposed to the cost of materials and labor, which can be affected by a wide range of events, including tariffs and immigration. Although home demand has been strong, the sector has suffered because of these risks.

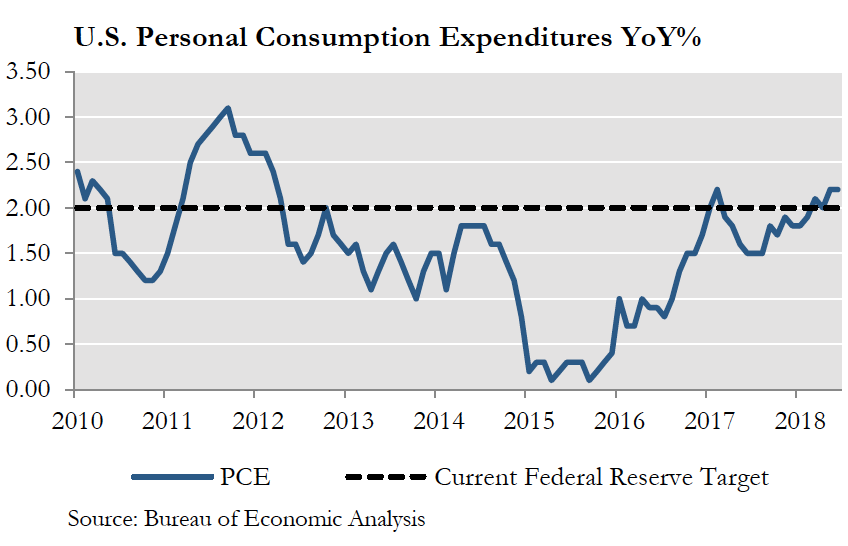

Additionally, for the first time since 2012, inflation is running at the Federal Reserve’s target (See Figure 4; PCE tracks overall price changes for goods and services purchased by consumers). Real assets, such as commodities and houses, tend to be the best performers in a higher inflation environment. Assuming inflation continues to lead commodities higher and labor costs continue to increase, home builder margins would compress if they are unable to raise their prices to keep pace, adding additional layers of ambiguity to the question of their forward value. As discount legacy non-agency RMBS are essentially interests in real assets, we believe they avoid many of these issues and offer some of the purest investor exposure to the U.S. housing market.

Recent data points, which have caused concern on the surface, show only a fraction of the total picture. Taking a step back provides a better view of the supply-demand dynamics. Negatives for home builders can actually be positives for U.S. home prices, dampening supply. Demand is growing, evidenced by steady growth in household formation and a homeownership rate that has finally turned the corner after 11 years of decline since its historic peak. Affordability, though off the highs, is still significantly above its pre-crisis average while real assets tend to show strong performance in rising inflation environments. Going forward, the supply-demand imbalance appears poised to persist and should be very constructive for not only the U.S. housing market, but for legacy non-agency RMBS as well.

Important Notes These materials have been provided for information purposes and reference only and are not intended to be, and must not be, taken as the basis for an investment decision. The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Ellington Income Opportunities Fund. This and other important information about the Fund are contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling 1-855-862-6092. The Prospectus should be read carefully before investing. Princeton Fund Advisors, LLC, and Foreside Fund Services, LLC (the fund’s distributor) are not affiliated. Investing involves risk including the possible loss of principal.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Ellington assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Ellington’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN STRATEGIES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN, INCLUDING INVESTMENT IN COMMODITY INTERESTS, IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS.

Example Analyses Example analyses included herein are for illustrative purposes only and are intended to illustrate Ellington’s analytic approach. They are not and should not be considered a recommendation to purchase or sell any financial instrument or class of financial instruments.

Forward-Looking Statements Some of the statements in these materials constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, estimates, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements in these materials are subject to inherent qualifications and are based on a number of assumptions. The forward-looking statements in these materials involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets in which we plan to trade; (ii) changes in strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in interest rates, the debt securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) increased prepayments of the mortgage and other loans underlying our mortgage-backed or other asset-backed securities; (viii) changes in governmental regulations, tax rates, and similar matters; (ix) changes in generally accepted accounting principles by standard-setting bodies; (x) availability of trading opportunities in mortgage-backed, asset-backed, and other securities, (xi) changes in the customer base for our business, (xii) changes in the competitive landscape within our industry and (xiii) the continued availability to the business of the Ellington resources described herein on reasonable terms.

The forward-looking statements are based on our beliefs, assumptions, and expectations, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of instruments and business discussed herein may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

PRINCF-20190924-0025