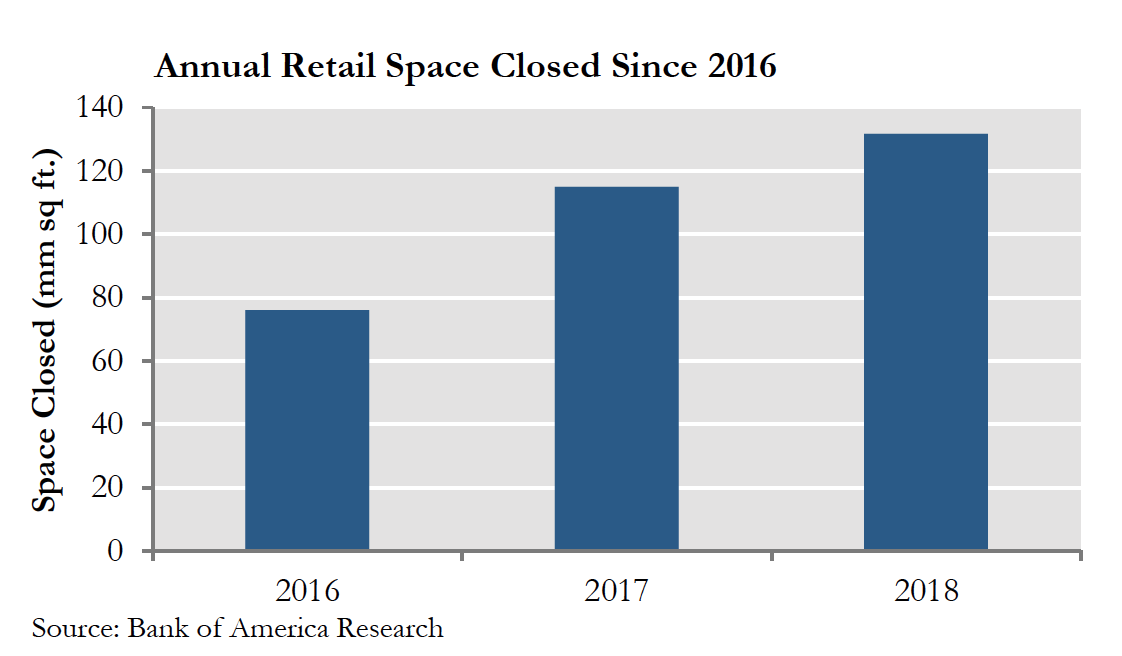

Retail bankruptcies and store closures have filled news headlines in 2018. Notable chains such as Toys-R-Us and Bon-Ton, ingrained in our culture and economy for decades, have gone into liquidation. Others such as Sears and Kmart have filed for bankruptcy after many years of weak performance. Store closure announcements seem to be a regular occurrence, even for healthy retailers. To put these statements into perspective, figures tabulated by Bank of America CMBS research show nearly 5,000 store closings in 2018 thus far, representing over 130 million square feet of retail space. In this piece we examine the current and future states of the retail sector along with the associated implications for the CMBS market.

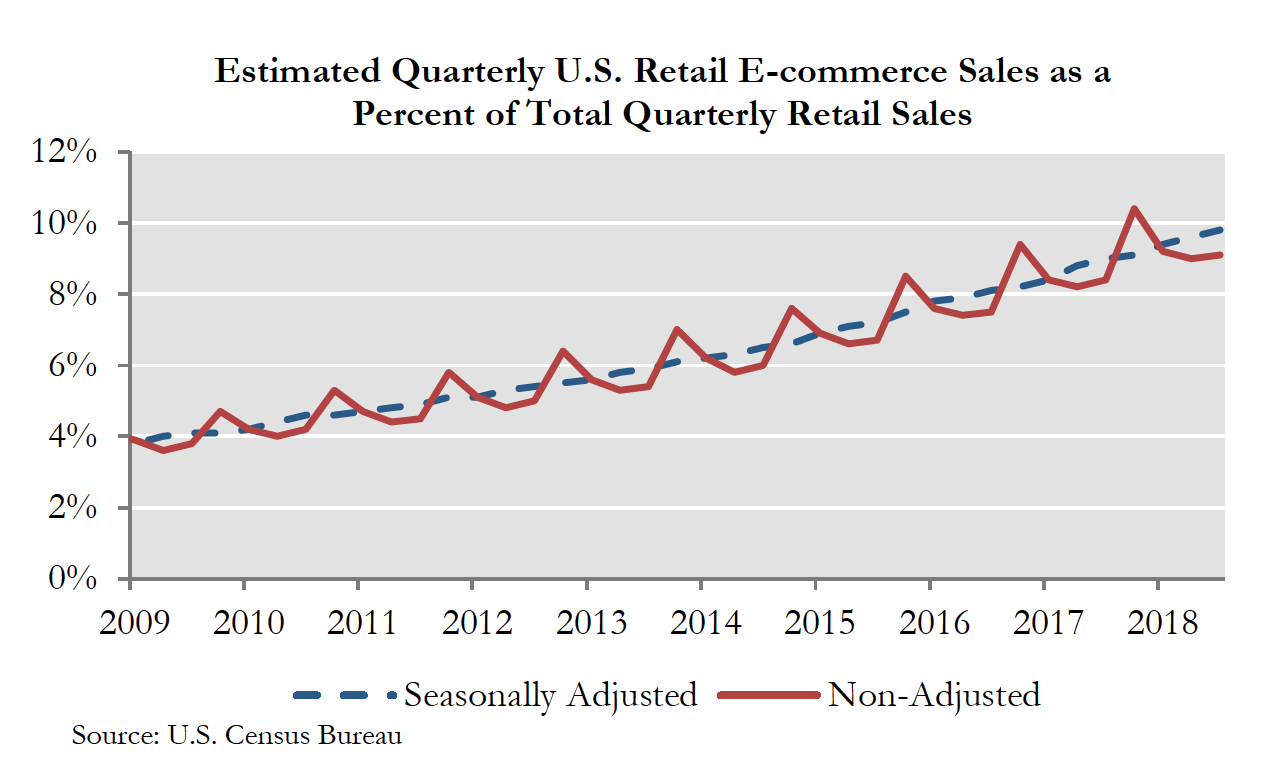

Retail has always been a dynamic segment of our economy. From Sears’ introduction of the mail-order catalog in the late 19th century to the growth of the suburban mall in the mid-20th century, the retail industry has relied on periodic reinvention to attract shoppers. With the rapid rise of e-commerce in the last decade, traditional retail stores have been forced to change at an even faster pace in order to maintain their relevance. JCPenney, for example, has experimented with the store-within-a-store concept, bringing Sephora into over 600 of its locations. Others, such as Neiman Marcus, have embraced Internet sales, with 36% of its 2018 fourth quarter sales generated online. Despite these attempts, however, the market share of online retailers has continued to increase over the last ten years, intensifying the challenge and creating a sense of urgency for their brick and mortar competitors. Online sales represented 9.8% of 2018 third quarter retail sales in the United States, with Amazon representing almost half of those online sales.

These trends have reduced the demand for physical retail space and have put retail tenants and their landlords under pressure. The Toys-R-Us bankruptcy resulted in 735 store closings this year, with Sears and Kmart closing 403 locations and counting. Bon-Ton’s liquidation resulted in 256 closures and the list continues well beyond these high-profile names. Retailer bankruptcies affect landlords by generating lease terminations and increasing anchor and in-line vacancies at properties. The tenants that do survive are emboldened to seek better terms at lease expiry or opportunistically based on their specific situation.

In some malls, the closure of an anchor may be an opportunity for a landlord to recapture a low-rent space and replace it with more productive tenants or to repurpose it entirely for a more popular restaurant/entertainment use that cannot be replaced by a few clicks online. This has meant adding restaurants such as The Cheesecake Factory, entertainment tenants such as Dave & Busters, and in some cases, even casinos to draw in foot traffic and shoppers. But this opportunity requires time and capital with landlords as with retailers, there are haves and have-nots. Simon Property Group, whose portfolio generates $650 per square foot in sales on average, has continued to grow rents by over 10% each year since 2012. On the other hand, CBL Properties, whose portfolio generates only $376 a square foot in sales on average, has struggled with annual rent declines of almost 7%.

While one closed anchor tenant may be an opportunity, two or more closed anchors could be an existential threat to the viability of a mall. Many mall tenants have “co-tenancy” clauses that allow them to lower rental payments or even terminate their leases if a certain number of anchors or percentage of mall occupancy is not maintained. The equity market has re-priced retail REITs downward given these risks and, in effect, limited their available capital. CBL, for instance, is down over 50% year-to-date.

From our perspective as a CMBS investor, these details make the underwriting of both the real estate and tenancy all that much more important. The old adage “location, location, location” still holds true to a large degree. A landlord can readily get a replacement tenant at workable rents in a prime location, even in the current environment. However, filling the weak locations in this retailer downturn has become uneconomic in many instances, as tenants and landlords face difficulty in finding a zone of agreement. Landlords in these weak properties face a dilemma as failure to invest capital puts a mall on the path to becoming a “dead mall” while investing capital risks deploying good money after bad if a viable lineup of retailers and tenants cannot be maintained. Thus, scarce capital is forced to flow to strong malls while “dead malls” are allowed to degrade. As a result, the weakest tier of malls has lost value the most rapidly and has produced eye-popping losses in CMBS trusts. As noted by Moody’s, six troubled malls were liquidated this past quarter at an average loss severity of 86.9%!

In general, cashflow stability is a main focus when we make CMBS debt investments. In addition to assessing property level sales productivity and rent costs on a loan-level basis, our underwriting also considers the credit profile of the underlying tenants. Many investors are rightfully concerned about lending against properties with a high percentage of short-term leases. However, we believe that investors often give too much credit to long-term leases in mitigating a property’s risk without considering the tenant’s ability to survive through the lease term. We are skeptical of long leases to tenants with negative cashflow, nearing debt maturities, or corporate debt trading at distressed levels. Instead of relying on stated lease maturities, we take a more nuanced view of longer-term tenants and carefully consider the impact of the loss of one or more tenants on the ability of a property to carry loan debt service.

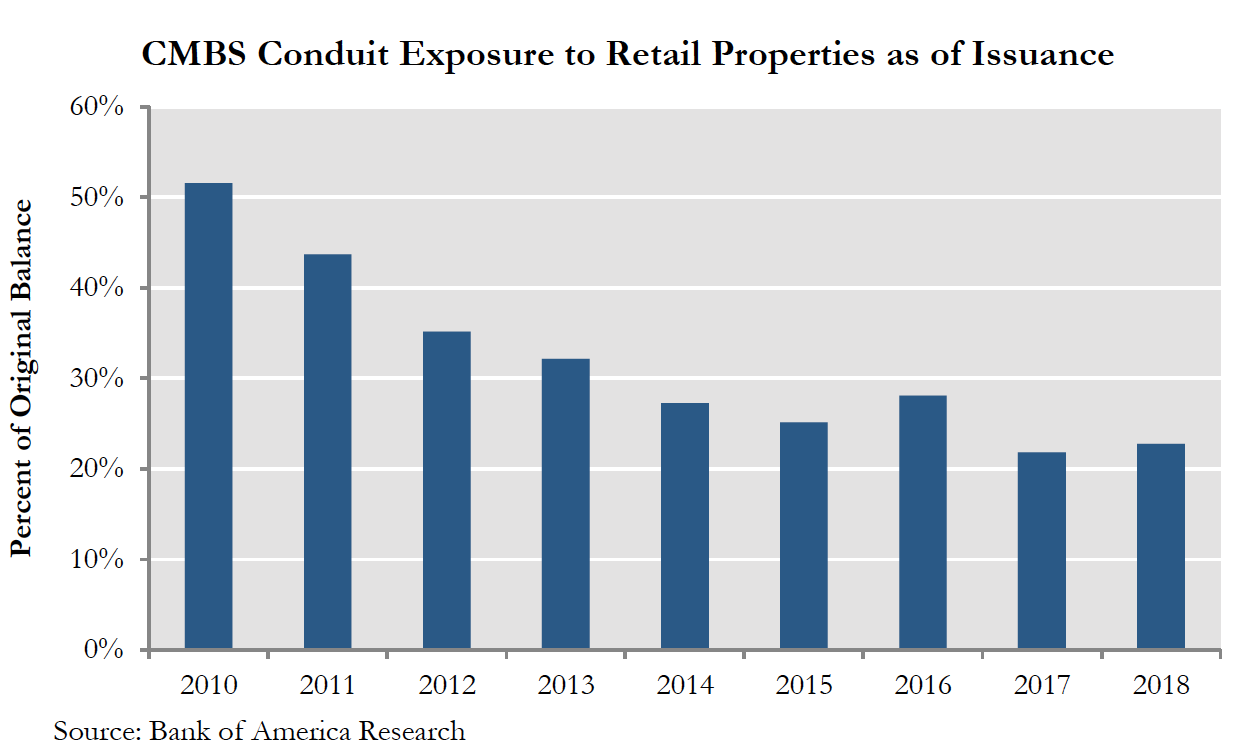

The inclusion of retail assets has decreased in CMBS over the last few years, which is unsurprising given the prevalent investor concerns regarding the sector. The more critical credit eye of the investor community has been a positive filter for pool composition in recent CMBS conduit deals, although the overall retail allocation is far from zero. While the inclusion of retail is something of a necessary evil within the CMBS conduit sector, it is much less widespread within the Commercial Real Estate (CRE) CLO sector. We have favored CRE CLO securities in recent months, especially in our lower risk funds, due to their floating rates, shorter durations, and significant amounts of credit enhancement, which are all very desirable characteristics in this turbulent market. Another added benefit of the CRE CLO sector is the minimal exposure to retail, which makes up only 7% of 2018 CRE CLO issuance, in contrast to 23% in 2018 conduit transactions.

Very few, if any, could have predicted the profound effects the Internet would have on all aspects of our lives during the past two decades. Similarly, we cannot readily predict the retail tenant landscape going forward, as change continuously seems to be happening at a more rapid pace. While we do not see retail going extinct (anytime soon, at least!), we recognize that the sector remains volatile and are managing portfolio composition accordingly.

Important Notes These materials have been provided for information purposes and reference only and are not intended to be, and must not be, taken as the basis for an investment decision. The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Ellington Income Opportunities Fund. This and other important information about the Fund are contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling 1-855-862-6092. The Prospectus should be read carefully before investing. Princeton Fund Advisors, LLC, and Foreside Fund Services, LLC (the fund’s distributor) are not affiliated. Investing involves risk including the possible loss of principal.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Ellington assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Ellington’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN STRATEGIES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN, INCLUDING INVESTMENT IN COMMODITY INTERESTS, IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS.

Example Analyses Example analyses included herein are for illustrative purposes only and are intended to illustrate Ellington’s analytic approach. They are not and should not be considered a recommendation to purchase or sell any financial instrument or class of financial instruments.

Forward-Looking Statements Some of the statements in these materials constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, estimates, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements in these materials are subject to inherent qualifications and are based on a number of assumptions. The forward-looking statements in these materials involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets in which we plan to trade; (ii) changes in strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in interest rates, the debt securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) increased prepayments of the mortgage and other loans underlying our mortgage-backed or other asset-backed securities; (viii) changes in governmental regulations, tax rates, and similar matters; (ix) changes in generally accepted accounting principles by standard-setting bodies; (x) availability of trading opportunities in mortgage-backed, asset-backed, and other securities, (xi) changes in the customer base for our business, (xii) changes in the competitive landscape within our industry and (xiii) the continued availability to the business of the Ellington resources described herein on reasonable terms.

The forward-looking statements are based on our beliefs, assumptions, and expectations, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of instruments and business discussed herein may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

PRINCF-20190924-0028