Tariffs and trade embargos have been a key piece of U.S. foreign policy for much of our history. From the nation’s founding through the early part of the 20th century, tariffs were regularly imposed to protect U.S. economic interests. While protectionist policies took a step back in the post-World War II era, they have come back strong under the current administration. Recently, President Trump has looked favorably upon tariffs as a tool for negotiating not only trade policy, but other issues such as immigration reform as well. So far, at President Trump’s direction, tariffs have been levied on $283 billion of U.S. imports, including a 25% levy on steel and a 10% levy on aluminum. There has been much concern in the markets that tariffs and the potential for a global trade war may cause more economic harm than good. In this piece, we examine the effect of tariffs on the U.S. economy, specifically the U.S. housing market, as well as the broader differences arising between structured credit and corporate credit in this new economic regime.

The question regarding the long-term effectiveness of tariffs raises controversy on both sides of the debate. While we won’t venture into that argument, it is clear that in the short-term tariffs can increase costs for consumers and businesses as well as create supply chain inefficiencies and economic uncertainty. The exact cost of tariffs on the economy is difficult to predict, but a few institutions have tried to quantify the amount. The Federal Reserve recently estimated that the current tariff regime will cost the U.S. over $100 billion per year, or $831 per American household. In other words, higher costs from tariffs have wiped out all but $100 of the $930 average tax cut that Americans received from the Trump administration last year.

While the higher cost of everyday goods can potentially increase default rates for consumers, the higher cost of housing can have a much more immediate effect on the structured credit markets. Tariffs impact the U.S. housing market in several ways. The most direct effect of tariffs is to increase the cost of materials used in the building of new homes. According to the National Association of Home Builders, tariffs will boost housing construction and renovation costs by $2.5 billion. Construction imports from China now carrying a 25% tariff include concrete, nails, screws, ceramic tiles, and roofing shingles, among others. In an already slowing housing market, increased prices of new construction can have devastating effects.

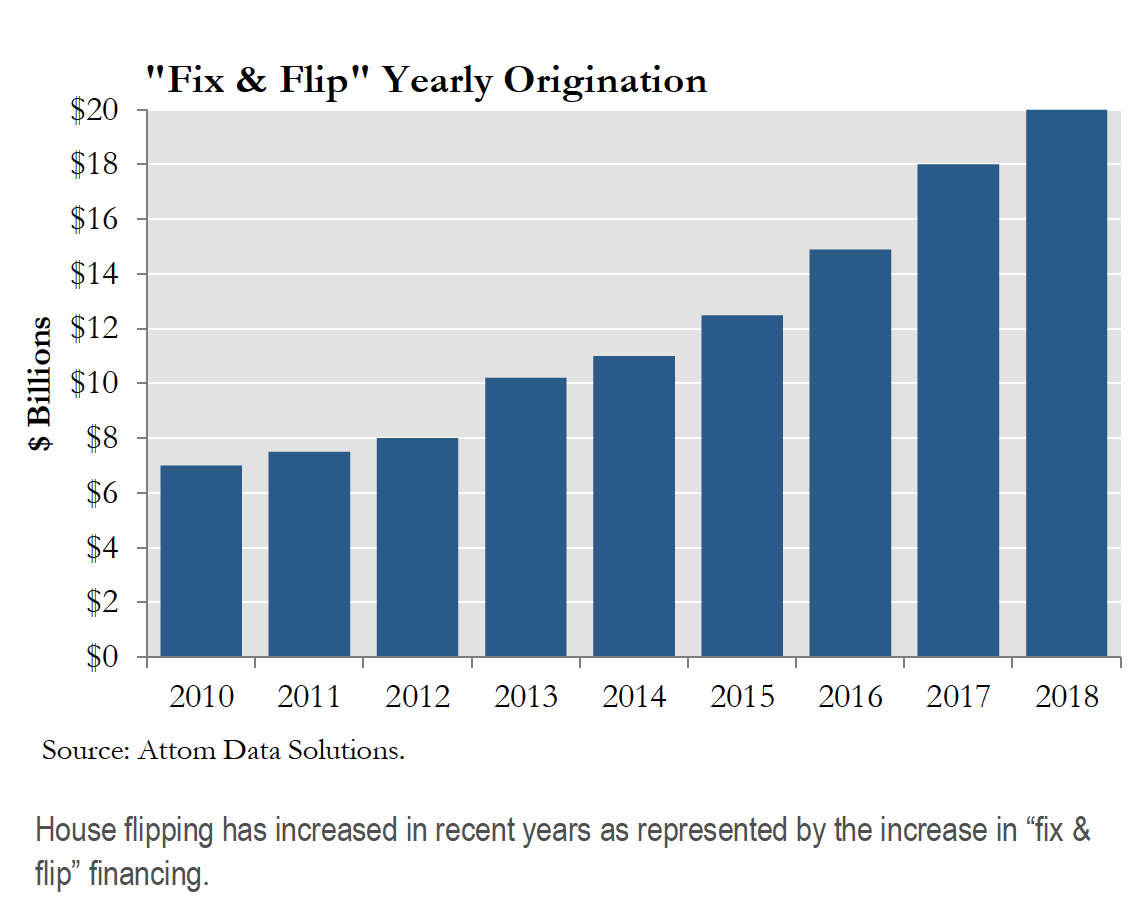

In addition to new construction, tariffs also impact the secondary home market. The “house flipping” market, which usually entails intensive renovations, has gradually become a larger portion of total U.S. home sales over the last several years. More than 200,000 homes were flipped in 2018, representing over 5.6% of all single-family home and condo sales. This was the third year in a row during which over 200,000 homes were flipped. Although the total number of homes flipped fell slightly last year, the 2017 total represented an 11-year high. The financing of these homes, in so-called “fix & flip” loans, grew to be a $19.9 billion industry in 2018. Many flippers, who already operate on very thin margins under normal circumstances, will feel squeezed from increased prices of construction and renovation goods, as well as home appliances, which are commonly replaced during the renovation process to boost a property’s selling price. The home appliance sector has been one of the most hard-hit by tariffs. Aside from higher prices of imported raw materials, President Trump has also targeted specific appliance sectors, such as his 20% tariff on imported washing machines.

Trade wars and retaliatory tariffs can also have a secondary effect on certain regional housing markets. To the extent that tariffs negatively impact regional-specific industries, they can depress home values in those locations. For example, China’s retaliatory tariffs on American agriculture goods could negatively impact farmers, who tend to be concentrated in certain areas of the country. The same can be said for auto and steel workers. Housing has traditionally been a regional market and when certain industries face a disproportionate negative impact, those local housing markets will suffer disproportionately as well.

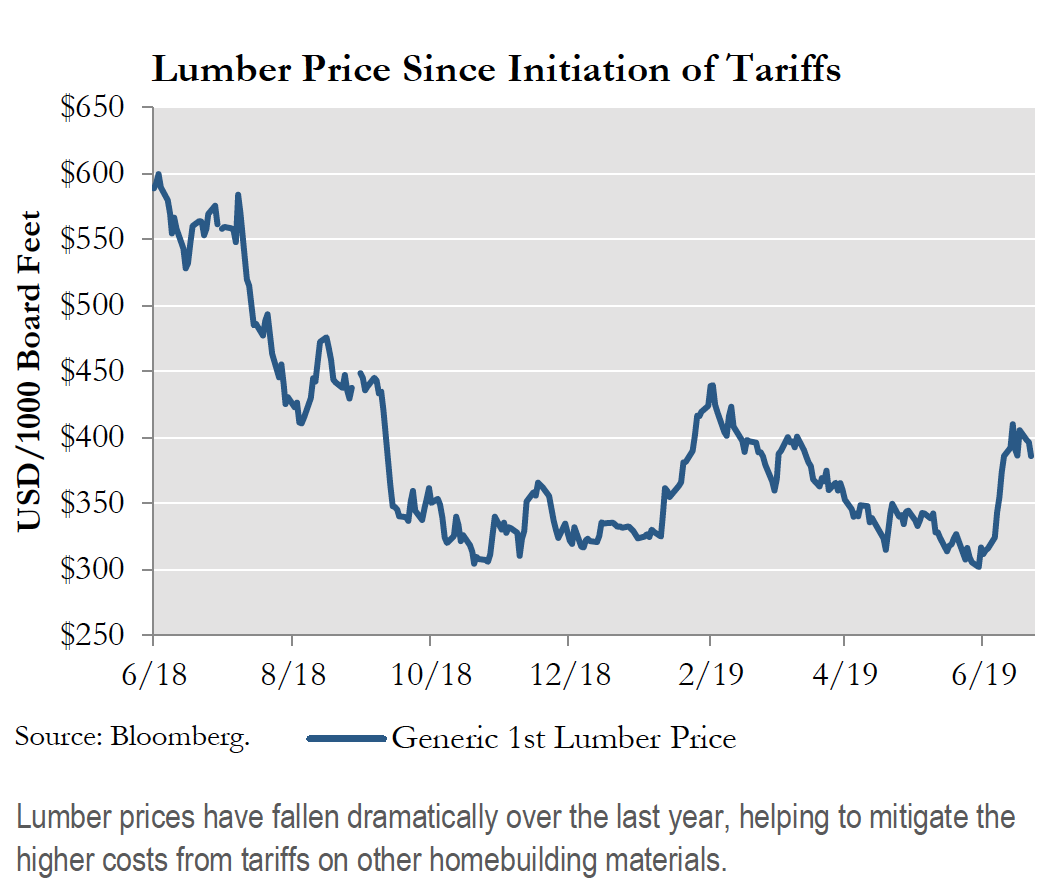

However, not all of the recent news is negative for homeowners. For one, the economic uncertainty that accompanies tariffs can keep interest rates low. The conforming mortgage rate has rallied over 120 basis points in the last seven months, improving home affordability in spite of higher building and renovation costs. Second, the cost of lumber has fallen significantly over the last year. While the tariffs on steel and aluminum have garnered some of the biggest headlines, these materials actually have a minimal impact on the cost of new houses since most new homes typically have more wood than metal. Whereas buying lumber represents one-third of the cost of building a new home, steel and aluminum contribute between 0.5% and 1.0% of a home’s cost. Although the price of lumber has risen in recent weeks, it is still approximately 40% lower than its mid-2018 highs, shortly after Canadian tariffs were instituted, further helping offset the negative impact of tariffs on the cost of new homes.

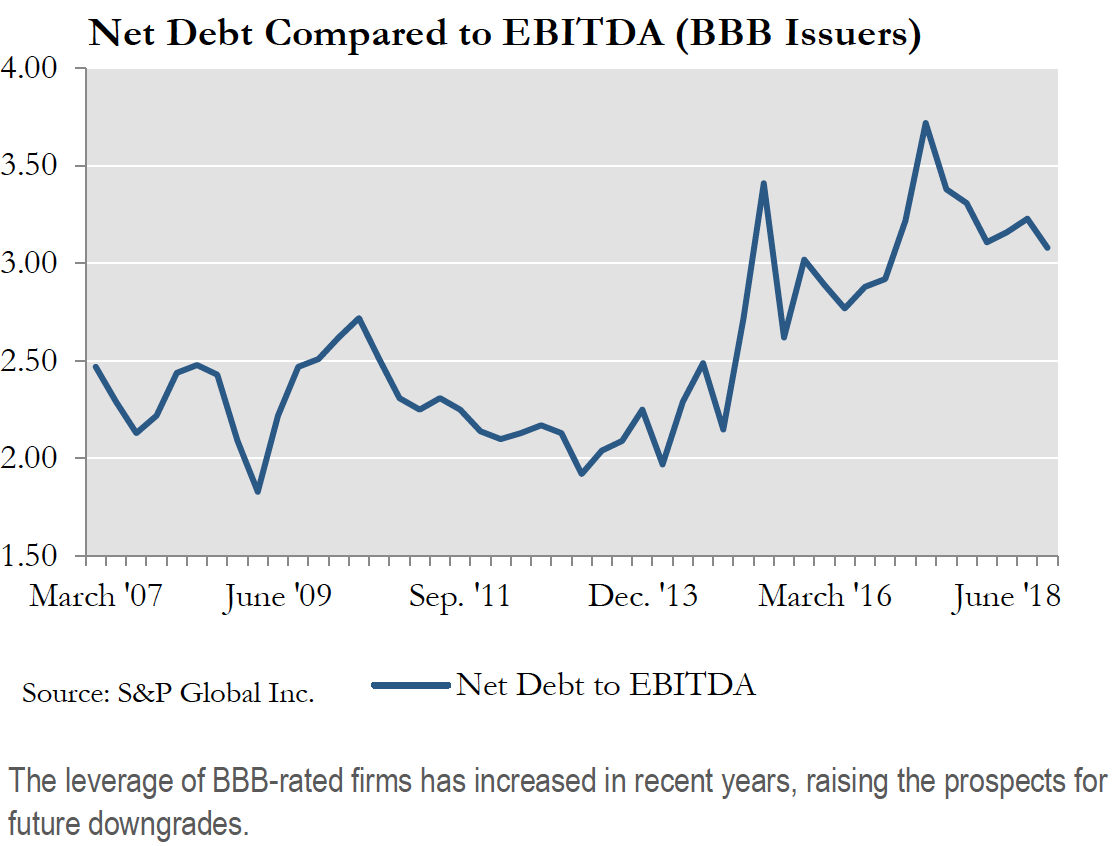

The current economic environment should also highlight the stability of structured credit assets in contrast to many of their corporate credit counterparts. Whereas the effects of tariffs on structured credit tend to be more evenly distributed among assets, they can create binary outcomes in corporate credit, where clear winners and losers tend to emerge. Firms such as oil pipeline manufacturers, heavily reliant on imported steel, emerged as losers while manufacturers of domestic fiberglass, a steel alternative, have benefitted from tariffs so far. With corporate leverage at an all-time high, downgrades and defaults could erupt very quickly, especially if a business faces a sudden impairment of cash flow or is forced to revamp its supply chain at a moment’s notice.

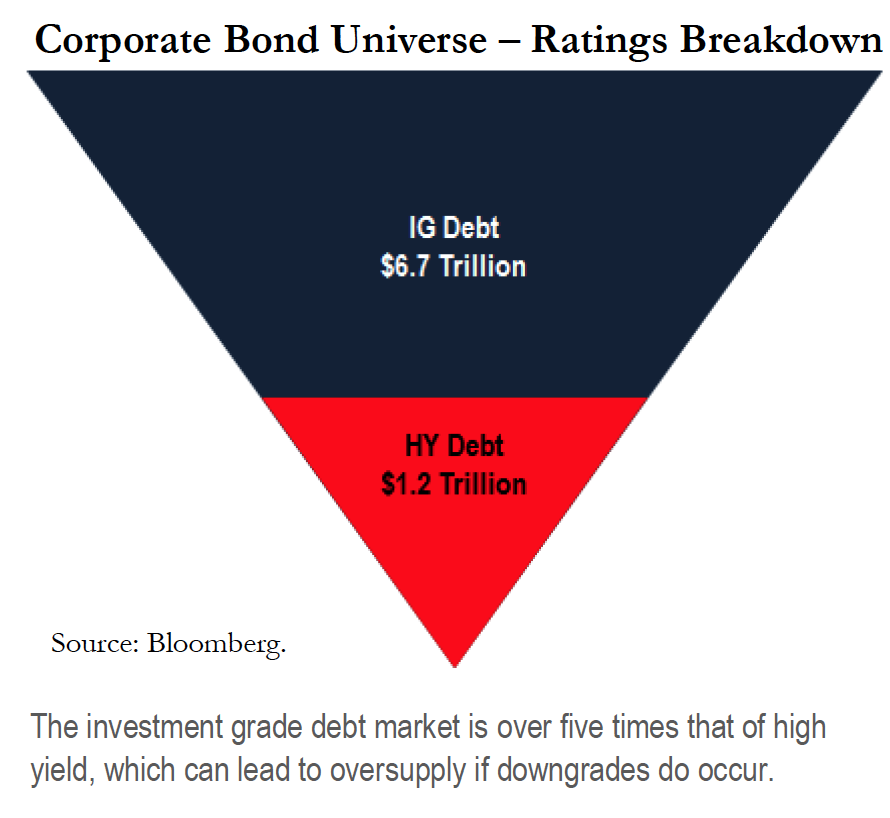

This is especially concerning in a market where the population of investment grade corporate bonds has gradually weakened over time. Currently, over 50% of the Bloomberg-Barclays Investment Grade Bond Index has some form of BBB rating, up from 35% before the 2008 financial crisis. With so many bonds teetering on the edge of investment grade, a slight uptick in downgrades could cause severe oversupply issues within the high yield market. Many managers have mandates to only purchase bonds with an investment grade rating, meaning there is little overlap between the buyer bases of both sectors. With over five times more investment grade corporate bonds than high yield securities outstanding, a small set of downgrades could send shock waves through the high yield markets where there aren’t as many managers to absorb the supply.

This is not an issue facing structured credit, especially legacy markets. The overwhelming majority of legacy non-agency RMBS are already rated below investment grade. Any further downgrades won’t impact the buyer base of those securities as they already have a mandate to invest in non-investment grade bonds. New issue securities with an investment grade rating come with a tremendous amount of protection, whether it is in the form of high credit enhancement from subordinate securities or more stringent underwriting standards on underlying loans. The rating agencies have been extremely conservative with investment grade requirements within structured credit as they seek to avoid another embarrassing situation like the mass downgrades that occurred during the last financial crisis.

The shift to a protectionist trade stance has impacted all aspects of the economy. Depending on the size and duration of the various trade wars, firms dependent on corporate debt markets that have outsized exposure to tariffs could be pushed towards a liquidity crisis. While there is no escaping the complete effect of tariffs, investors can limit their exposure through proper asset allocation. With a President who does not seem to be changing his stance any time soon, investors should re-visit structured credit as an attractive alternative.

Important Notes These materials have been provided for information purposes and reference only and are not intended to be, and must not be, taken as the basis for an investment decision. The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Ellington Income Opportunities Fund. This and other important information about the Fund are contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling 1-855-862-6092. The Prospectus should be read carefully before investing. Princeton Fund Advisors, LLC, and Foreside Fund Services, LLC (the fund’s distributor) are not affiliated. Investing involves risk including the possible loss of principal.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Ellington assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Ellington’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN STRATEGIES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN, INCLUDING INVESTMENT IN COMMODITY INTERESTS, IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS.

Example Analyses Example analyses included herein are for illustrative purposes only and are intended to illustrate Ellington’s analytic approach. They are not and should not be considered a recommendation to purchase or sell any financial instrument or class of financial instruments.

Forward-Looking Statements Some of the statements in these materials constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, estimates, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements in these materials are subject to inherent qualifications and are based on a number of assumptions. The forward-looking statements in these materials involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets in which we plan to trade; (ii) changes in strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in interest rates, the debt securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) increased prepayments of the mortgage and other loans underlying our mortgage-backed or other asset-backed securities; (viii) changes in governmental regulations, tax rates, and similar matters; (ix) changes in generally accepted accounting principles by standard-setting bodies; (x) availability of trading opportunities in mortgage-backed, asset-backed, and other securities, (xi) changes in the customer base for our business, (xii) changes in the competitive landscape within our industry and (xiii) the continued availability to the business of the Ellington resources described herein on reasonable terms.

The forward-looking statements are based on our beliefs, assumptions, and expectations, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of instruments and business discussed herein may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

PRINCF-20190924-0034