In the years immediately following the 2008 financial crisis, the availability of consumer credit tightened dramatically. As a result, the personal balance sheet of the average American improved as consumers were forced to de-lever in the absence of financing options. However, while mortgage credit issuance, the largest form of consumer credit, came to a virtual halt immediately after the crisis, auto lending remained elevated. A recent increase in auto loan delinquencies has caught the eye of many in the structured credit investor community. Does this portend a significant pullback in consumer credit or is it a small, explainable blip in an otherwise strong economy? In this piece, we examine the history of auto lending in the post-crisis era as well as examine the potential reason for the elevated delinquencies.

Interestingly, auto delinquency rates did not increase to levels anywhere near mortgage delinquencies during the financial crisis. Many borrowers, in dire financial conditions at the time, simply made the decision to continue to pay their car loans over other forms of consumer credit, including their mortgage payments. While counterintuitive at first, the decision is actually very rational. In many parts of the country, cars are a necessity for everyday life, including commuting to and from work. Without a car, many would not be able to maintain a job. Unlike homes, cars can be quickly repossessed if a borrower falls seriously behind on their payments, leading borrowers to prioritize those payments over others.

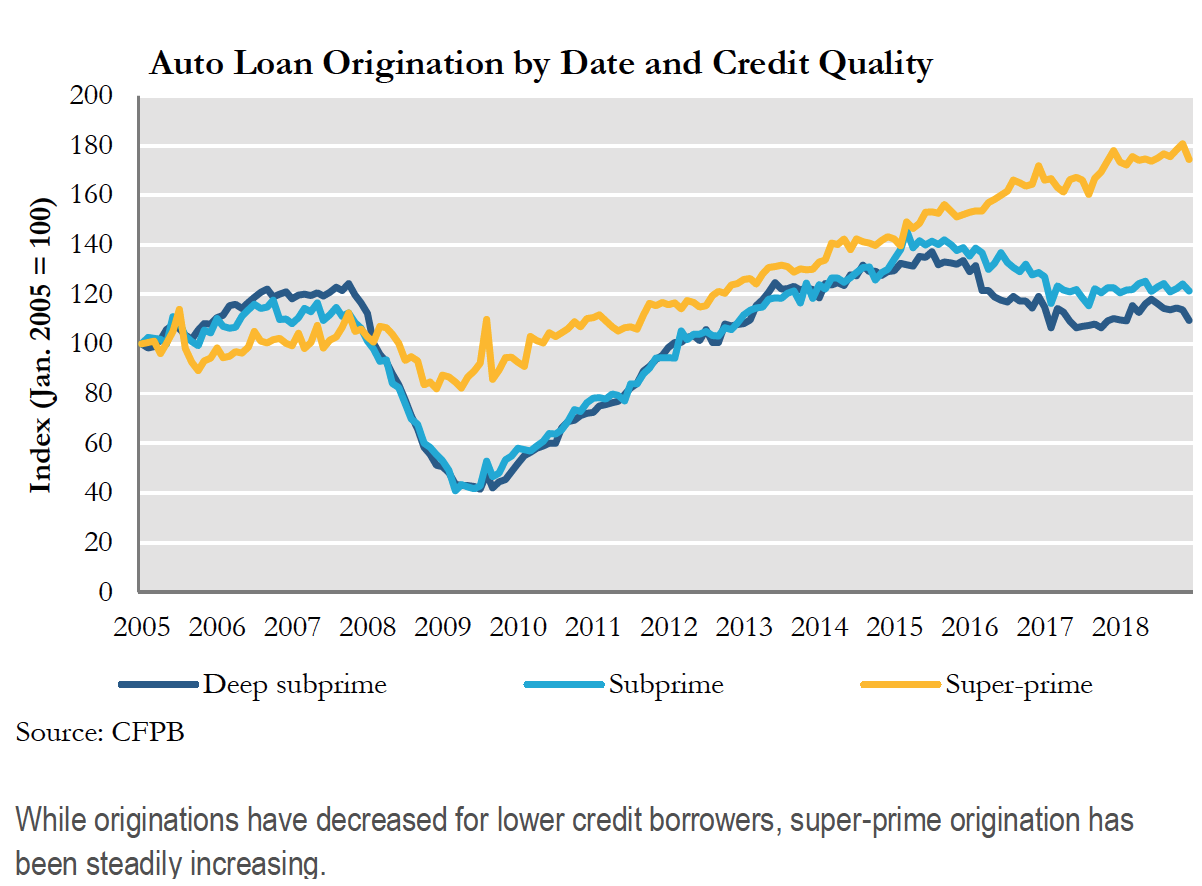

The relatively stable performance of the sector is one reason that issuance remained robust in the post-crisis era. Auto loan origination has grown to a $1.3 trillion market in recent years, up from $800 billion immediately preceding 2008. This growth has been partially fueled by an influx of private equity capital, as buyout firms poured billions into subprime auto lending in an attempt to capture profits from the sector’s high interest loans. For example, Blackstone invested almost $500 million in Exeter Finance, a subprime auto lender operating in all 50 states, beginning in 2011. Subprime auto loans (defined as borrowers with < 620 FICO scores) and deep subprime (loosely defined as a subset of subprime borrowers with <580 FICO) now make up 20% of the market. Auto loans are typically originated through two main channels – banks/credit unions and auto-finance (non-bank) companies. While a large portion of the loans are kept on balance sheet, approximately $60 billion are securitized and syndicated to investors each year.

Delinquencies in the sector began to pick up in late 2014 and have continued to steadily increase. According to recent dealer research, over 7 million borrowers are currently more than 90 days delinquent on their auto loans. To put this in perspective, only 1.5 million borrowers were at the same level of delinquency in 2000. Even adjusting for the increased amount of loan volume today, the rate at which borrowers are going delinquent is over two times higher than it was at the beginning of the century. In fact, the overall auto delinquency rate is only approximately 0.5% lower now than it was at its peak in the years immediately after the financial crisis.

Not surprisingly, these elevated levels of delinquency have led to concerns about consumer credit in general. Is the auto loan sector a harbinger of what is to come in other areas of structured credit? As of now, the answer appears to be no. The data simply does not indicate any large scale pullback in overall consumer performance. Outside of a small increase in credit card delinquencies, consumer performance has actually remained quite strong. In fact, mortgage and student loan delinquencies have actually fallen over the last several years.

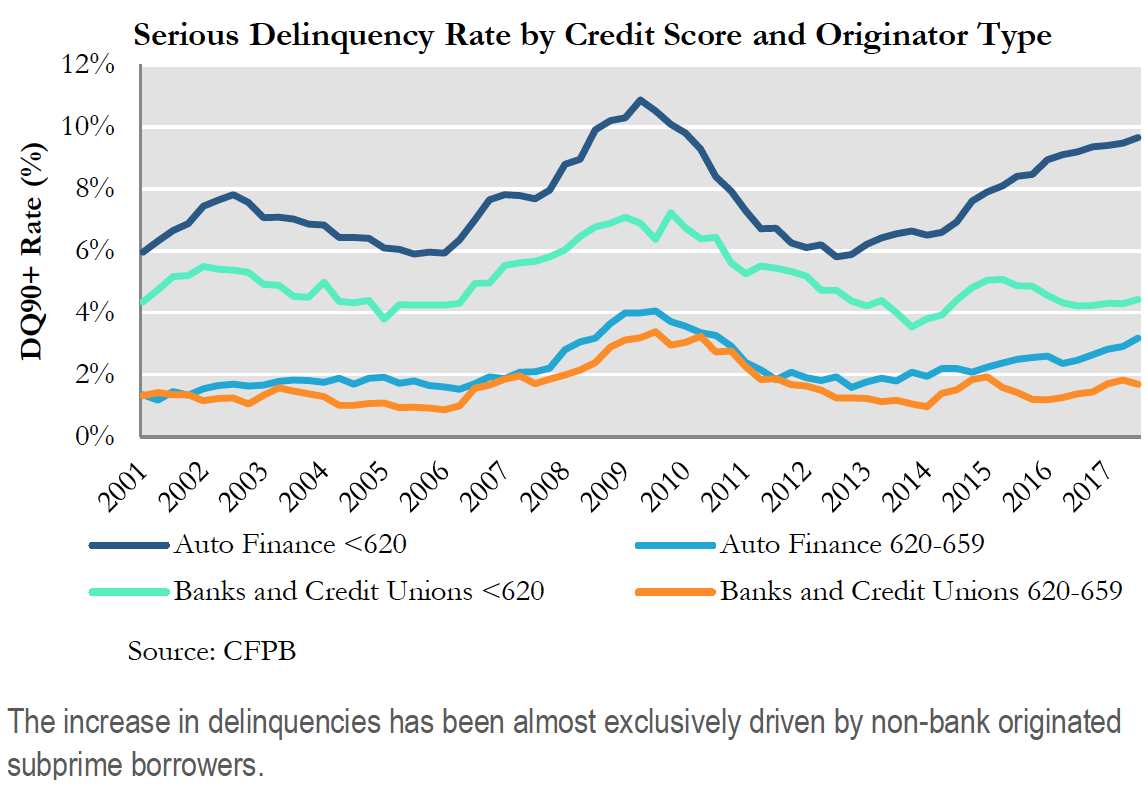

Instead, the rise in auto delinquencies can be attributed to one particular pocket of the market. Subprime and deep subprime borrowers, specifically those originated through auto finance companies, are responsible for most of the recent uptick in delinquencies. The performance of prime borrowers has remained extremely stable, with originations actually growing in recent years for very clean, super-prime borrowers.

The poor performance of subprime and deep subprime borrowers may not be attributed to a weakening of borrower fundamentals, but rather to an overexpansion of credit. During the post-crisis years, non-bank originators gradually expanded their credit box to include borrowers at the bottom of the credit score distribution curve. Origination to subprime and deep subprime borrowers peaked in late 2015. However, after a rash of defaults, the credit box quickly tightened for non-bank originators. Since 2015, total inquiries for new auto loans have remained relatively stable, but inquiries that don’t result in a new transaction are up 7%. The overwhelming majority of these inquiries come from the subprime and deep subprime pool of borrowers.

Although performance has recently stabilized for lower credit borrowers, the market has already felt significant effects. Several non-bank auto finance companies, such as Summit Financial, have filed for bankruptcy, while others, such as Pelican Auto, have halted originations. Many other non-bank originators, including Spring Tree and Honor Finance, have faced various types of financial difficulties. However, as more non-bank originators who catered to the low credit segment leave the market, overall lending standards have become tighter, which benefits the performance of the sector as a whole.

While the downturn in lower credit auto performance had serious implications for non-bank originators, the impact on securitizations was minimal. For one, only around 15% of subprime auto origination is in securitized form. While those deals had high loss rates, they also had significant excess spread from high interest rates on the loans that provide additional cushion against losses to bondholders.

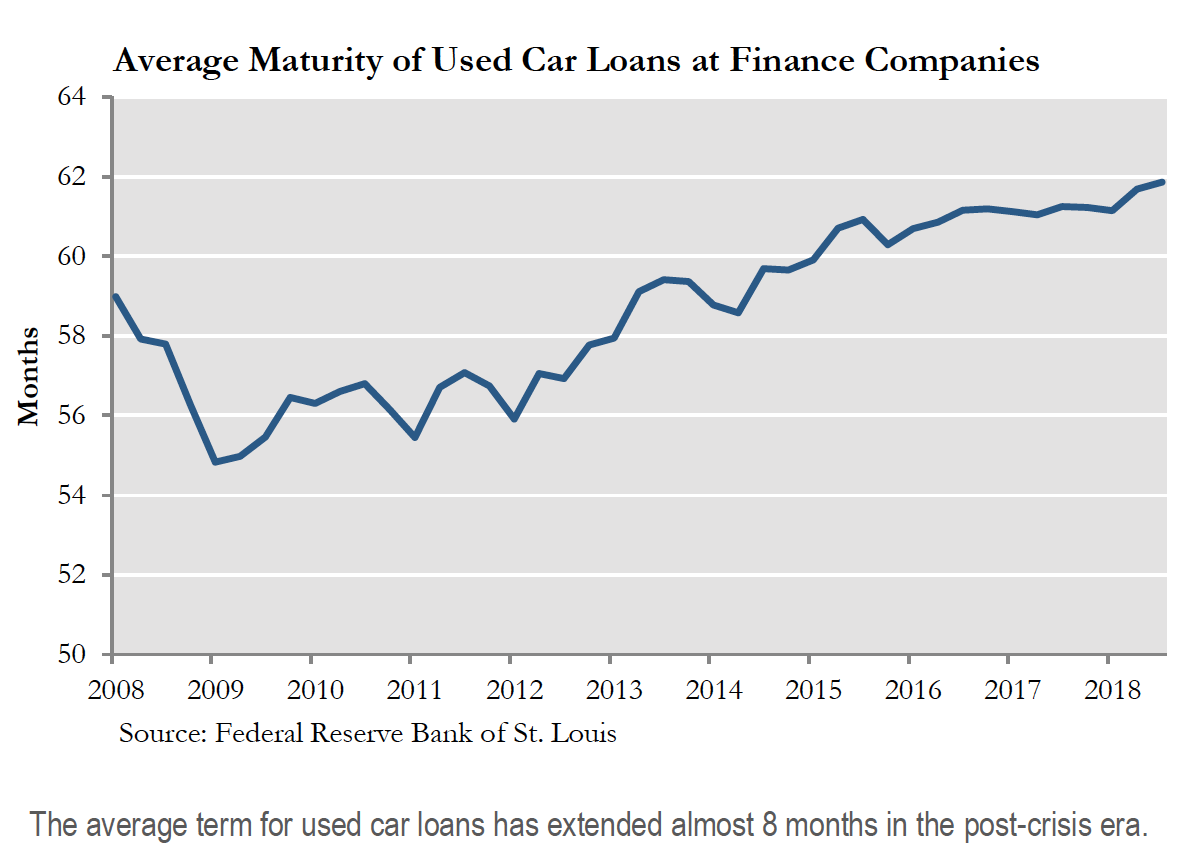

Although these bonds have layers of loss protection mechanisms, we still believe investors should take caution, especially with regards to the term of the underlying loans. Even as the credit box has tightened in terms of borrower credit quality, loan terms have gradually increased. These increased terms could pose a problem, especially in light of the aged vehicles backing the loans. Regardless of borrower credit score, this mismatch between loan term and the lifespan of the associated vehicle should be a focus of investors going forward.

U.S. consumers remain the beneficiary of a tight labor market and wage growth. While the elevated levels of auto delinquencies in recent years are concerning, they appear to be the result of lenders overextending credit to borrowers who simply should not have received a loan in the first place. This overextension and subsequent pullback of credit is typical within a market and appears to have been righted without serious consequences reverberating through the economy.

Important Notes These materials have been provided for information purposes and reference only and are not intended to be, and must not be, taken as the basis for an investment decision. The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Ellington Income Opportunities Fund. This and other important information about the Fund are contained in the Prospectus, which can be obtained by contacting your financial advisor, or by calling 1-855-862-6092. The Prospectus should be read carefully before investing. Princeton Fund Advisors, LLC, and Foreside Fund Services, LLC (the fund’s distributor) are not affiliated. Investing involves risk including the possible loss of principal.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Ellington assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Ellington’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN STRATEGIES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN, INCLUDING INVESTMENT IN COMMODITY INTERESTS, IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS.

Example Analyses Example analyses included herein are for illustrative purposes only and are intended to illustrate Ellington’s analytic approach. They are not and should not be considered a recommendation to purchase or sell any financial instrument or class of financial instruments.

Forward-Looking Statements Some of the statements in these materials constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, estimates, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward-looking statements in these materials are subject to inherent qualifications and are based on a number of assumptions. The forward-looking statements in these materials involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets in which we plan to trade; (ii) changes in strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in interest rates, the debt securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) increased prepayments of the mortgage and other loans underlying our mortgage-backed or other asset-backed securities; (viii) changes in governmental regulations, tax rates, and similar matters; (ix) changes in generally accepted accounting principles by standard-setting bodies; (x) availability of trading opportunities in mortgage-backed, asset-backed, and other securities, (xi) changes in the customer base for our business, (xii) changes in the competitive landscape within our industry and (xiii) the continued availability to the business of the Ellington resources described herein on reasonable terms.

The forward-looking statements are based on our beliefs, assumptions, and expectations, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of instruments and business discussed herein may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

PRINCF-20190924-0031